Overcoming DI Objections: “No thanks, I’ve got disability insurance through work.”

President | OneProtection

Michael.Sir@OneProtection.tech

As seen in Aspire Magazine, March 2024.

Often times when an insurance agent or financial advisor brings up the topic of disability insurance (DI) to a client they hear, “I already have disability insurance through work.”

Unfortunately, most advisors don’t know how to handle this objection, so they simply move on to the next topic leaving this important area of planning unresolved.

Instead of letting them continue to “think” they have coverage, show them what that “coverage through work” (group long-term disability insurance) actually provides.

Starting the disability insurance conversation

Before you even start the DI conversation with your client, try to find out what kind of group disability insurance their employer offers (i.e., short-term vs long-term) including the plan details. This information will help you confidently handle the rest of the discussion.

When you know what their employer offers, from a group disability perspective, you can take a more active approach to starting the DI conversation. For example you can start by saying, “I see that [their employer] already provides you with group disability insurance. Let’s go through what that actually means so there are no surprises should you have a health event and we can see if you need to supplement that coverage.”

The client will most likely agree that it’s a good idea and then you’re on your way to having the DI (Income Protection) conversation.

Use the TRIPP method to help explain how the employer coverage works.

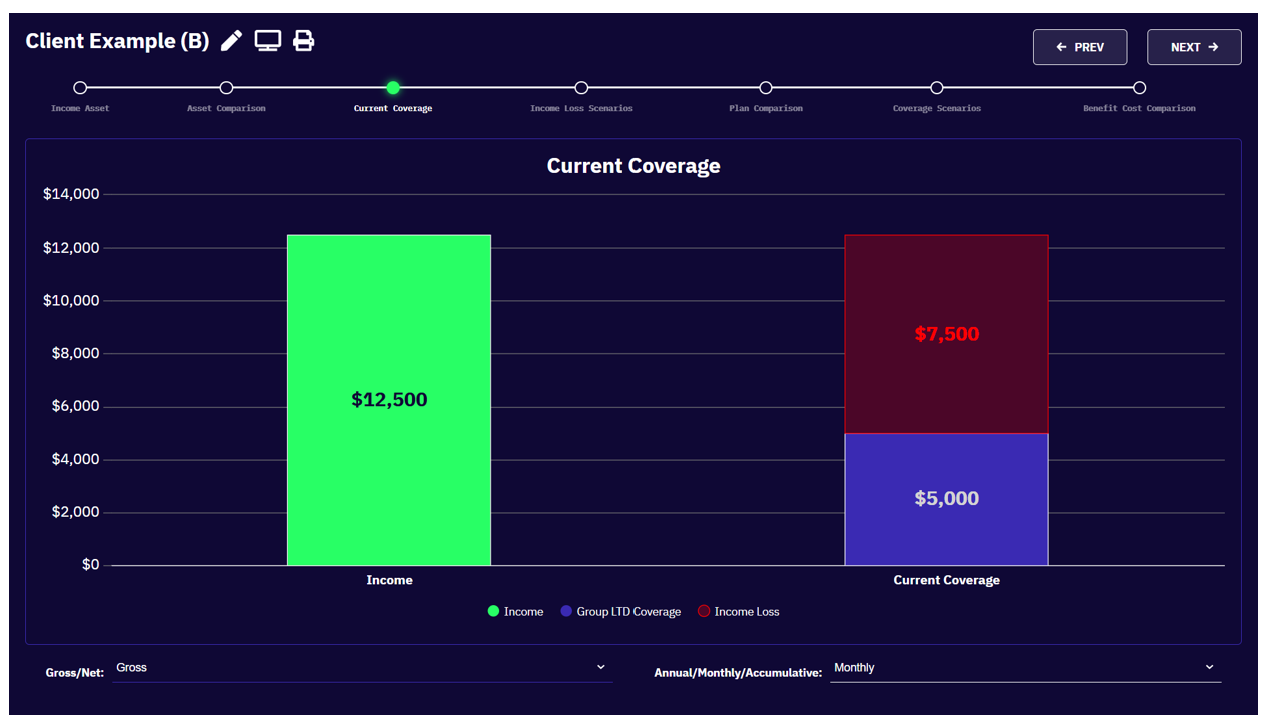

For this exercise let’s assume you have a client/prospect that is age 35 and is making $150,000 per year ($12,500/month) and their annual income is both a $100,000 salary and $50,000 of bonus. The Group long-term disability (LTD) plan covers 60% of covered earnings up to $7,500/month.

T- Taxable. If the Group LTD is paid for by the employer and the employee is not responsible for any of the premiums, it is called a Non-Contributory plan.

This means the employee doesn’t contribute to the cost, which is really good news that their employer cares enough about the employees to provide this valuable benefit.

The bad news is the benefits would be taxable during a claim. So, the best-case scenario is the employee would have a 40% pay-cut right out of the gate.

Most employees have no idea this is the case and are not prepared to handle this monthly shortfall. Especially since their expenses are likely to increase due to COBRA premiums, deductibles, co-pays, uncovered medical expenses, travel and other treatment related expenses, etc.

R-Reverse Discrimination. This term is normally used when the advisor is having a conversation with the employer. However, what it means is the employee is making more than the Group LTD covers.

In this example, the client makes $150,000 (or $12,500/month pre-tax). Their Group LTD covers 60% up to $7,500/month, pre-tax.

The Group LTD is designed to cover a wide variety of employees in the company and for those that make more than $150,000 (of covered earnings), they may need additional coverage to make sure the higher income earners aren’t discriminated against.

I-Incentive Compensation. Employees and business owners are paid in a number of different ways (salary, bonus, hourly, overtime, commissions, K-1, partnership earnings, etc.).

The question here is what is definition of “Covered Earnings” in the Group LTD plan.

Many Group LTD plans only cover salary or base wage and don’t cover the other types of compensation. In our example, only the $100,000 salary is covered leaving the bonus uncovered compensation.

This is a major problem as the actual replacement percentage isn’t 60% of income but rather 60% of Salary which would result in only 40% of total compensation in this example. And, then the Group LTD benefits are taxed so it’s a double whammy.

P-Provisions. There are many provisions inside a group LTD plan that can impact the benefits paid. Some of the most important provisions include:

- Own-Occupation – How long is the employee covered in their own-occupation. Many Group LTD plans have a 2-year own-occupation definition and then it becomes any reasonable occupation thereafter. Some have own-occupation protection for the full benefit period. The definition of occupation is important, and the advisor should explain what this means.

- Offsets – One of the biggest misunderstandings is that of Social Security or Workers Compensation benefits. If the employee is disabled and receives benefits from either or both of these sources, the Group LTD benefit will “offset” these benefits and the Group LTD benefit will be reduced. This is almost always an unwelcome surprise as the employee was expecting these benefits to be paid in addition to their Group LTD benefit.

- COLA – A Cost of Living Adjustment is an optional provision that few employers provide. It allows the benefits to increase, while they’re disabled, over time to keep up with inflation. COLAs are rare in the group LTD world. It’s expensive so most employers don’t buy this provision for their employees. Therefore, when on claim, the buying power of the monthly benefit without a COLA will erode over time.

- Mental, Nervous and Substance Abuse (MNSA) coverage. Most group LTD plans have a 24-month limitation for MNSA claims and will only continue after that period if the claimant is hospital confined.

P-Portability.

Who owns the group LTD plan? The answer is, well, no one. It’s an employee benefit that is provided by the employer for the employee while the employee is working at that company.

If the employee were to terminate employment, for whatever reason, they leave behind their Group LTD coverage.

Employees leave employers all the time and employers are letting employees go as well so it’s important for your client to understand that group LTD is not owned or controlled by the employee. It is therefore not guaranteed that they will have coverage if they were to need it down the road.

Now that we’ve taken our client on our TRIPP, now what?

Pivot the conversation to how the client can protect more of their income by supplementing their Group LTD coverage with Individual Disability Insurance.

The combination of employer-paid Group LTD and a personally-owned Individual DI policy is the most effective way to protect your client’s most valuable asset…their ability to make and grow their income over the course of their working years.