A guide to actuarial techniques in R and Python

An actuary is a professional who applies statistical and mathematical methods to assess risk, especially in insurance, finance, and other industries. Actuaries implement a broad range of techniques to assess the likelihood of future events, plan for outcomes, and mitigate risks.

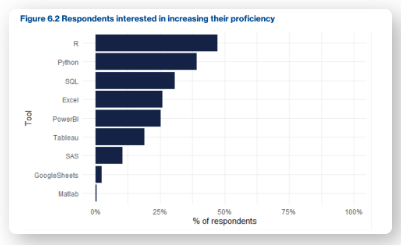

Back in 2022, the Casualty Actuarial Society released the First Annual CAS Actuarial Technology Survey. The survey asked 1,294 actuaries which tools they use, their self-reported proficiency levels, the barriers they experience, which techniques they apply, and in which areas they would like to improve.

The survey revealed that R and Python were the top two tools actuaries were most interested in learning:

Why could this be? We believe it is because coding offers significant advantages over traditional spreadsheet-based methods:

- Reproducibility: Models built with code can be run over and over again with the exact same result.

- Transparency & auditability: Every calculation and assumption is explicitly written out in the code to make it easy to review and audit.

- Scalability: Scripts can handle massive datasets and complex calculations that would be difficult in a spreadsheet.

Using coding languages means less processing time and no need to copy/paste, recreate prior model values, or wait for vendor support. In short, coding saves time and increases accuracy. Don’t just take it from us, though. Dr. Maria Prokofieva, professor at the Victoria University Business School in Australia, shares a detailed overview in her blog post, R is for actuaRies.

Let’s explore some core actuarial techniques and see how they can be implemented using R or Python.

Loss Reserving: The Chain-Ladder Method

Loss reserving is a fundamental actuarial task that involves estimating the ultimate cost of insurance claims that have already occurred but have not yet been fully paid. One of the most common techniques is the chain-ladder method. This deterministic method uses historical claim development patterns to project future claims.

Implementing it in code offers a major advantage: automation. You can easily apply the method to hundreds of different business lines simultaneously, something that would be tedious and error-prone in a spreadsheet.

Both R and Python have excellent libraries for this:

- R: The ChainLadder package provides functions for performing the chain-ladder calculation and other related reserving methods, including the ability to apply the Bornhuetter-Ferguson method, which is a variation that combines the chain-ladder approach with an initial expected loss ratio.

- Python: The chainladder package offers a similar suite of tools.

Pricing: Generalized Linear Models (GLMs)

Actuarial pricing involves determining the appropriate premium for a policy based on the risk it represents. Generalized Linear Models (GLMs) are the industry standard for this task. They allow actuaries to model the relationship between a dependent variable (e.g., claims costs) and various independent variables (e.g., age, policy type, location).

GLMs are an extension of simple linear regression that can handle non-normal data, such as claim counts (which are often Poisson-distributed) or claim severities (which can be gamma-distributed).

R is a favorite among actuaries for statistical modeling, and it has an incredibly robust ecosystem for GLMs. The base R glm() function is the go-to tool.

Modeling Loss Distributions: Excess Loss Analysis

Excess loss analysis is a key technique in reinsurance and large-scale insurance. It focuses on the distribution of losses that exceed a specific threshold (or deductible). This analysis helps actuaries price “layers” of risk: the amount a reinsurer is responsible for paying above a certain limit.

The actuar package in R is an essential tool for this kind of work. It provides functions to fit and analyze loss distributions, such as the Pareto, Lognormal, or Gamma distributions, which are all commonly used to model high-severity claims.

Looking ahead

As actuarial work becomes more data-intensive and complex, the adoption of coding languages will become an even more critical skill. We believe that the ability to write clean, reproducible, and scalable code will become a core competency for the modern actuary.

Check out the R Resources for Actuaries & Insurance Analysts from the R Consortium to continue your journey.

How Posit can help

Actuarial models are essential for assessing financial risk by projecting the impact of future events. Posit helps actuaries overcome challenges with data silos and clumsy legacy tools by providing a modern, code-first environment to build more accurate and easily validated models.

Discover how Posit helps leading insurance companies accelerate insights, manage risk, and drive innovation.